Rising Tide of Credit Card Debt: Impact on Credit Score

Are you ready to take control of your financial future? Building credit doesn’t have to be stressful or complicated. With the right credit builder card, you can strengthen your credit history safely, affordably, and without surprises.

Why Choose a Credit Builder Card?

Unlike traditional credit cards that often come with high interest rates and the risk of overspending, a credit builder card is designed with one goal—helping you grow your credit score responsibly.

Safe & Secure – Bank-level security protects your personal information.

No Credit Check – Start building credit without worrying about past history.

Reports to All 3 Bureaus – Equifax, Experian, and TransUnion all receive your payment history.

With this card, you’re not just borrowing—you’re building.

How It Works: Simple Steps to Better Credit

Apply in Minutes – A quick 2-minute application with no credit check.

Fund Your Card – A refundable $200 deposit secures your account and helps avoid late payments.

Use & Build – Make small everyday purchases, pay on time, and watch your score rise.

Many users see score increases of 50+ points with consistent, responsible use.

Why Your Credit Score Matters

Your credit score impacts almost every financial decision—from buying a home to getting a car loan, making it crucial to pay your bills on time. Here’s how much your score could save you on various sectors of the economy, particularly regarding higher rates on loans.

Home Loan Example ($200,000, 30-Year Fixed): a finance option that can help you manage your credit card debt.

- Score 630 → $156,054 interest, $989/month

- Score 760 → $92,563 interest, $813/month, which can hinder economic growth if not managed properly.

That’s a $63,491 savings just by having better credit.

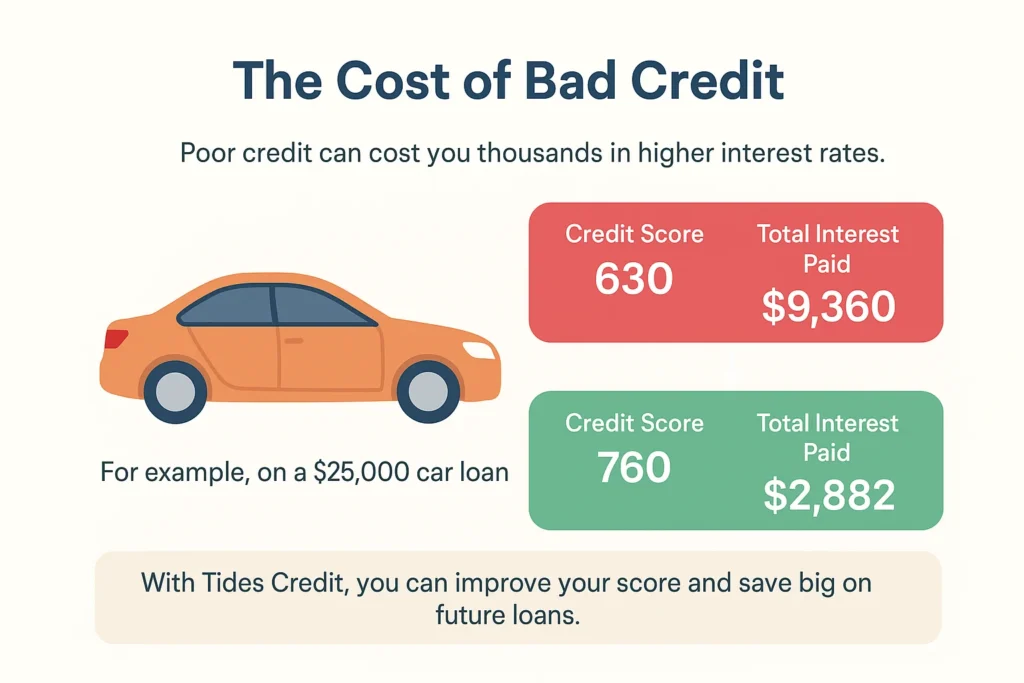

Auto Loan Example ($30,000, 60 Months):

- Score 630 → $9,492 interest, $658/month

- Score 760 → $2,882 interest, $548/month

That’s $6,610 saved on the same car.

A strong credit score means lower interest rates, lower monthly payments, and more money in your pocket.

Credit Builder Card vs. Traditional Credit Cards

| Feature | Traditional Credit Card | Credit Builder Card |

|---|---|---|

| Interest Rates | Often over 30% | Under 25% |

| Credit Limits | High, tempting overspending can lead to overdue bills if individuals do not manage their credit card balances, especially with the current economic landscape. | $200, keeps you in control |

| Reporting Speed | 30+ days of delinquency can severely impact your credit report. | Reports within a week |

| Goal: to reduce levels of credit card delinquency. | Lender profit | Your credit success |

This card is built to help you succeed, not trap you in debt.

Real Stories, Real Success

Our customers have transformed their lives with Tides Credit. Here’s what they’re saying:

“In just three months, Tides Credit helped me remove negative accounts and fix late payments. Their team is amazing, and the customer service is top-notch!”

– Justin Y., 5 stars (Facebook)

“I thought bankruptcy was my only option, but Tides Credit proved me wrong. My score is climbing, thanks to their guidance!”

– Meriah G., 5 stars (Facebook)

“From a 600 to a 740 score! Tides Credit made it happen, and I’m blown away by the results.”

– Josh W., 5 stars (Google)

“Tides Credit helped me buy my dream car! Their team was patient, professional, and always there to answer my questions.”

– Ashlee L., 5 stars (Google)

“Kane and the Tides team are dedicated and hardworking. They tailored a plan for me, and now my credit has unlocked new possibilities!”

– Taylor G., 5 stars (Google)

Why Trust Us?

100,000+ users already building credit.

8 years of proven results in helping individuals reduce their card debt in the United States.

85% say it’s the easiest way to start building credit.

Your card ships in as little as 2 weeks after deposit funding, allowing you to use credit cards responsibly. And yes—your $200 deposit is fully refundable.

Struggling with Debt?

If you’re weighed down by high-interest credit card balances, you’re not alone. In 2025, U.S. credit card debt crossed $1 trillion, creating financial stress for millions of households. Minimum payments, rising interest rates, and late fees keep borrowers stuck in a cycle of debt.

But there’s a way out—starting with building positive payment history and improving your credit score to avoid penalties.

Explore Pismo’s Latest Whitepaper

Want deeper insights into the future of credit? Pismo’s latest whitepaper reveals how U.S is rapidly adopting credit card usage. Stay informed about digital innovations and emerging credit trends to manage their credit card transactions effectively., reshaping the lending landscape. From mobile-first solutions to smarter underwriting, these changes point toward a future where borrowers can manage their credit card balances and succeed financially.

The Alarming Numbers

- Average U.S. household credit card balance: $7,800

- Average interest rate on new credit cards: over 20%, contributing to the rising tide of credit card debt.

- Millions of cardholders are paying thousands extra in accumulating interest each year due to overdue payments and mismanaged credit card balances.

These numbers highlight why building strong credit early can save you from significant financial strain later in the current economic landscape.

Broader Economic Implications

Rising debt levels don’t just affect individuals—they ripple through the economy. High consumer debt reduces overall spending power, slows economic growth, and increases risks for banks and lenders. Policymakers are left balancing inflation control with the rising tide of credit card debt while needing to support borrowers.

Contributing Factors

Several key drivers are fueling the surge in credit card debt in the United States, including rising credit card interest rates.

- Rising cost of living is a significant factor contributing to debt in the United States. – Rent, food, and healthcare are climbing faster than wages.

- Easy access to credit – Quick approvals and flashy rewards encourage overspending, which can hinder financial stability.

- The minimum payment trap – Covering only interest while debt lingers.

- Financial literacy gaps – Many borrowers don’t fully understand credit score impacts.

Recognizing these factors is the first step to avoiding debt traps.

FAQs for rising tides credit card

How soon will I get my card?

About 2 weeks after your deposit is funded and approved, you may receive information about potential annual fees.

How much can my score improve?

Many users see gains of 50+ points with on-time payments and low usage.

Is there a credit check?

No. Only a refundable $200 deposit is required.

What makes this card different?

Unlike other secured cards, this one reports quickly, charges low annual fees, and focuses on helping you build—not borrow endlessly, improving your ability to secure future credit.

How many people have $10,000 in credit card debt?

Roughly 1 in 10 U.S. households carry $10,000 or more in credit card debt. With the national average balance around $6,000, anyone with $10,000 is well above average and paying thousands more in interest every year due to higher rates.

What is the 2/3/4 rule for credit cards?

The 2/3/4 rule is an unofficial guideline for applying for new credit cards issued by various issuers:

No more than 2 cards every 30 days can lead to increased credit card interest rates if not managed wisely, making it crucial to pay bills on time.

No more than 3 cards every 90 days can tighten your financial health if not managed properly.

No more than 4 cards every 12 months

It helps prevent too many hard inquiries, which can hurt your credit score.

Is Chase Rise a good credit card?

Chase Rise is still a relatively new product, designed for consumers who want to build or rebuild credit while accessing Chase’s rewards ecosystem. It may be a good option if you want to start with a trusted bank, but the benefits depend on your financial goals, spending habits, and credit profile.

How bad is credit card debt right now?

Credit card debt in the U.S. has hit an all-time high of over $1 trillion, prompting many to seek ways to manage their credit card balances. Credit card debt in the U.S. has hit an all-time high of over $1 trillion, with a significant uptick in cards in circulation.. Rising interest rates, inflation, and the minimum payment trap are making it harder for households to pay balances in full and manage their credit card balances effectively. Many borrowers are struggling with higher financial stress and delayed goals like buying a home or car.

Are you tired of feeling overwhelmed by credit card debt?

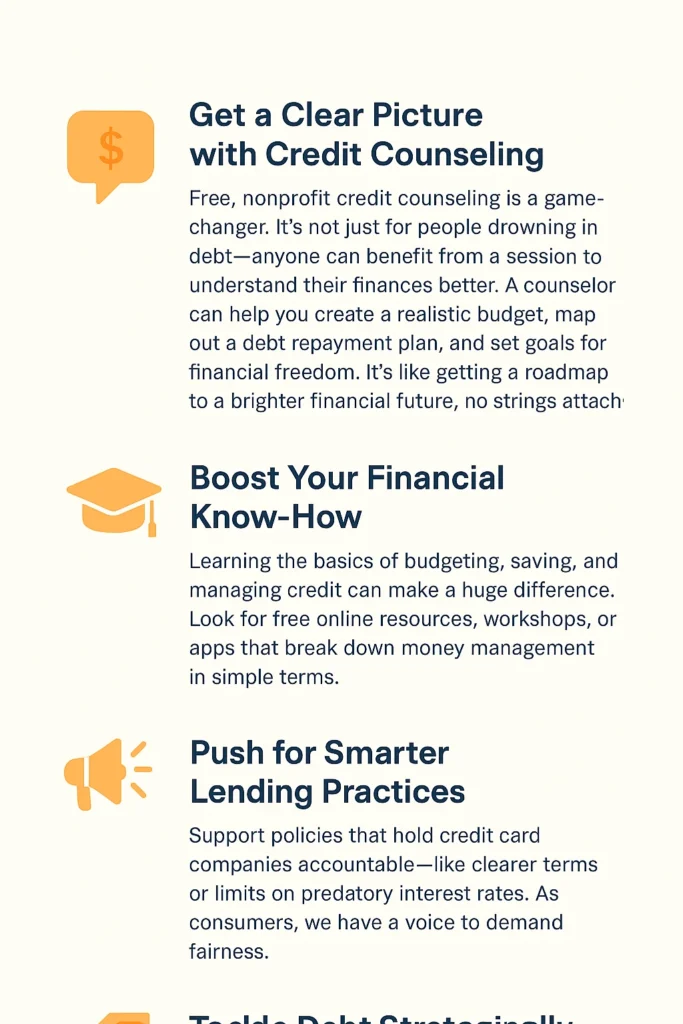

If credit card debt feels overwhelming, you’re not alone; many are facing similar challenges in managing online shopping expenses. The good news is, there are solutions. Options like credit counseling, debt consolidation, balance transfer cards, or a secured credit builder card can help you regain control. The key is to start with a plan and take one step at a time.

Has the US ever defaulted on its debt?

Technically, the U.S. has never fully defaulted on its debt. However, in 1979, a small technical delay caused missed Treasury bill payments due to a paperwork glitch. Otherwise, the U.S. has always met its debt obligations, even during financial crises.

How does making a minimum payment impact the pace at which your credit card debt is paid off?

Paying only the minimum balance keeps your account in good standing, but it barely reduces the principal. Most of your payment goes toward interest, meaning it could take years or even decades to pay off your balance. Whenever possible, pay more than the minimum to save money and get out of debt faster.

What state are you looking to purchase in?

This question usually comes up when applying for a mortgage, car loan, or insurance. Lenders ask which state you’re purchasing in because loan terms, taxes, and insurance rules vary by state. Knowing the location helps them give you accurate rates and options.

What if I told you that mastering credit card debt is simpler than you think?

It’s true—credit card debt feels complex, but the basics are simple: spend less than you earn, pay more than the minimum, and keep your balances under 30% of your limit. Tools like balance transfers, secured cards, or debt snowball methods can speed up progress.

Will credit card debt elevate financial stress levels to the point where consumer spending slows down even more dramatically, potentially jeopardizing the economy?

Yes, if debt keeps rising, households may cut back on non-essential spending, which drives much of the U.S. economy. Slower spending reduces business growth, lowers hiring, and can trigger broader economic slowdowns. That’s why managing consumer debt is important not just for individuals, but for various sectors of the economy as a whole, especially in 2022.

The Bigger Picture: Why Credit Building Matters

In 2023, U.S. credit card debt passed $1 trillion—that’s nearly $7,800 per household. High interest rates, rising living costs, and the minimum payment trap are leaving many borrowers stuck in debt, tightening their financial health.

But you can break the cycle. By using a credit builder card wisely, you establish positive payment history, keep balances low, avoid accumulating interest, and create a stronger credit profile that helps you secure loans, mortgages, and better financial opportunities.

Take the First Step Toward a Stronger Financial Future

The easiest way to start improving your credit score is by building positive history today, which can help offset high credit card usage. With a Credit Builder Card, you get a simple, affordable, and secure tool designed to unlock your financial goals.

Apply now and start building your credit with confidence, and enjoy free credit monitoring.

Key Takeaways

What is the easiest way to build credit fast? → Use a secured credit builder card and pay on time.

Do credit builder cards really work? → Yes, they report to all three credit bureaus and can raise scores by 50+ points.

How much deposit is needed to avoid high credit card interest rates? → $200, fully refundable.

Can I get approved with bad credit? → Yes, no credit check required.

As a seasoned loan and credit card expert, I have an in-depth understanding of the financial industry, specializing in helping individuals and businesses navigate the complexities of borrowing and credit. My expertise spans across various loan types, including personal, business, auto, and mortgage loans, as well as credit card products, enabling me to provide tailored advice and solutions. With a focus on optimizing financial health, I guide clients in making informed decisions that align with their goals, ensuring access to the best terms, rates, and strategies for managing credit and debt effectively.

Leave a Reply